This article is for educational and informational purposes only and is not financial or medical advice. Consult a qualified financial professional before making changes to your financial plan.

Financial Wellness Without Hustle Culture

Why financial wellness is about breathing room, not becoming your own private equity firm.

What Is Financial Wellness, and Why Does It Have Nothing to Do with Hustle?

What does financial wellness actually mean?

Financial wellness is the state of having enough stability, margin, and control over your money to make choices rather than react to emergencies. According to the Consumer Financial Protection Bureau, financial well-being means you can meet current and ongoing financial obligations, feel secure about your financial future, and make choices that let you enjoy life. It does not require six income streams, a passive-revenue course, or waking up at 4 a.m. to grind. It requires clarity, consistency, and enough breathing room to sleep at night.

Key Takeaways

Financial wellness is defined by stability, margin, and the ability to make choices, not by wealth accumulation or side-hustle income.

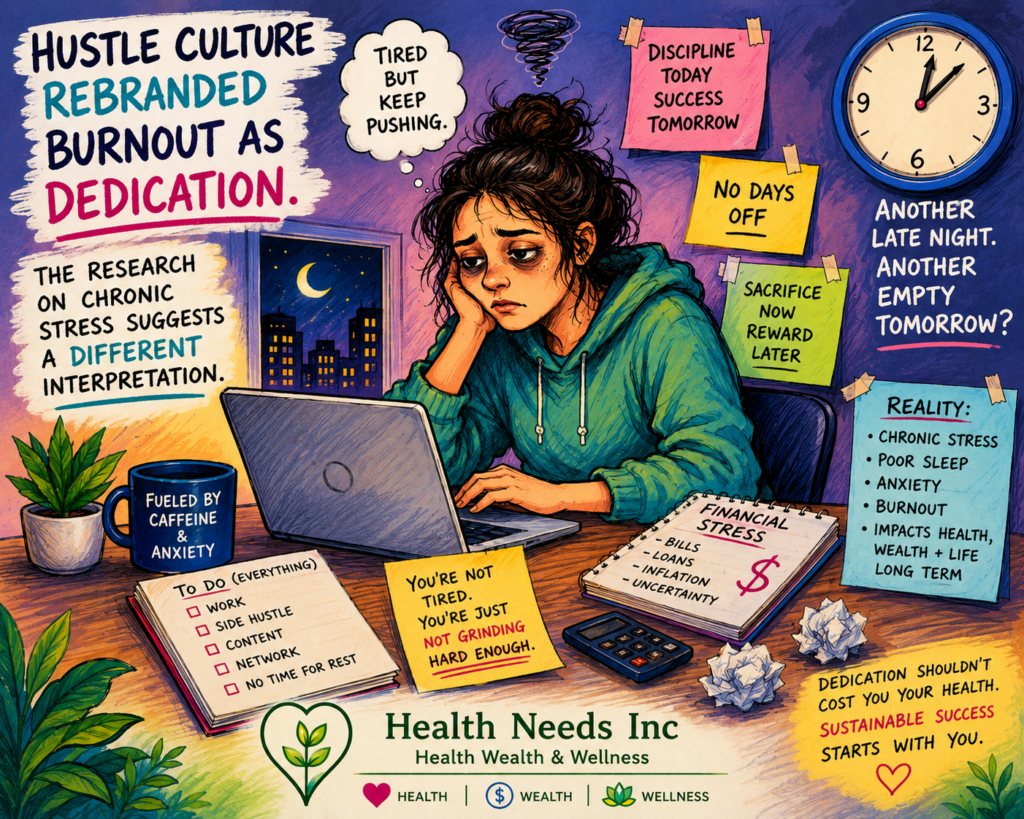

Hustle culture rebranded exhaustion as ambition, turning productivity into a moral virtue and rest into laziness.

Hedonic adaptation means more income does not automatically reduce financial stress. Lifestyle expands to absorb the raise.

An emergency fund is as much a psychological tool as a financial one. Savings buys calm.

The best financial plan is the boring one you will actually follow. Consistency beats sophistication across every time horizon.

The useful financial question is not “am I winning?” but “am I okay?” The second question actually has an answer.

The Confusion at the Heart of Financial Wellness

You mention enjoying photography and immediately a stranger on the internet suggests selling presets, creating courses, and building passive income streams. You post pictures of homemade cookies and someone asks why you have not turned it into a six-figure side hustle. Financial wellness, somewhere along the line, got confused with perpetual motion.

The message simplified down to: work harder, wake earlier, optimize everything, build seven income streams, sleep when you are dead. If that sounds less like wellness and more like an unpaid internship with capitalism, you are not alone. The wellness industry has a long and distinguished history of repackaging anxiety as aspiration, and financial wellness content is no exception.

But financial wellness without hustle culture is not some radical new idea. For most of human history, the goal was not infinite productivity. It was stability. Enough. A life that was not constantly on fire. That is worth rediscovering, and it turns out the research agrees.

The Consumer Financial Protection Bureau defines financial well-being as having control over day-to-day finances, the capacity to absorb a financial shock, being on track to meet financial goals, and having the freedom to make choices that allow enjoyment of life. Four criteria. Not one of them mentions passive income.

What follows is a clear-eyed look at what financial wellness actually requires, what hustle culture sold us instead, and how the boring path is almost always the right one. Financial wellness is just one of eight dimensions of wellness that shape how we function, but it interacts with all the others in ways that are easy to underestimate.

Financial Wellness Is Not Wealth

The wellness industry loves complicated frameworks. Financial influencers are no different. They will sell you a system involving color-coded spreadsheets, ten investment accounts, and a morning routine that apparently begins at 4:12 a.m. while reading philosophy books in an ice bath.

Financial wellness is remarkably boring. And boring is underrated.

Financial wellness is not owning three rental properties by thirty-five. It is not retiring on a yacht while posting inspirational quotes with a sunset backdrop. The actual definition is simpler and more useful: Can you pay your bills? Do you sleep at night without calculating what breaks next? Do unexpected expenses ruin your month, or merely inconvenience it? Can you make choices instead of constantly reacting to emergencies?

People often chase wealth when what they actually want is relief. The distinction is not semantic. Chasing wealth means the target keeps moving. Chasing relief means there is actually an arrival point. Research on income and subjective well-being has consistently found that the relationship between money and happiness flattens at a certain threshold, once basic needs and a modest buffer are covered. A 2021 study in PNAS found emotional well-being rises with income but does not plateau as sharply as earlier research suggested, though the relationship is far from linear. The relevant point is this: the gains from going from stressed to stable are massive. The gains from going from comfortable to wealthy are marginal, and they come at a cost.

How Hustle Culture Sold Anxiety as Ambition

Hustle culture arrived dressed as empowerment. Who could object to ambition? Who does not want opportunities? The trouble started when productivity became a moral virtue and rest became its absence.

Rest became laziness. Vacations became weakness. Leisure became wasted potential. The phrase “rise and grind” transformed into a personality. And beneath all the motivational posters sat a strange assumption: if you are exhausted, you are doing life correctly.

Nobody says: look at that person with chronic burnout and elevated cortisol, they must really have their priorities straight. Yet financially, exhaustion became a badge of honor. Working eighty hours a week was not a warning sign. It was something to put in your bio.

The result was millions of people trapped on a treadmill that never stops moving. The problem with treadmills is that speed and direction are not the same thing. Chronic stress triggers sustained cortisol elevation, which affects sleep quality, cognitive function, and cardiovascular health, regardless of how many income streams the person running on the treadmill has managed to build. Financial anxiety and financial wellness are not compatible states.

Why More Income Does Not Automatically Create More Wellness

Income matters. Pretending otherwise would be insulting. Financial stress is real, measurable, and consequential. Chronic money worries affect sleep, anxiety, relationships, and physical health in ways that have been well-documented by researchers for decades.

But beyond meeting essential needs, something interesting happens. Lifestyle expands. Expectations rise. Expenses quietly mutate.

The raise arrives. Then comes the larger house payment. The upgraded car lease. The streaming subscriptions multiplying like rabbits. Furniture somehow becomes an identity. Before long, yesterday’s luxuries have become today’s necessities. Psychologists call this hedonic adaptation. Normal people call it “where did all my money go?”

The research on hedonic adaptation is well-established. A foundational study by Brickman, Coates, and Janoff-Bulman demonstrated that lottery winners returned to near-baseline happiness levels within a year. More recent work has confirmed the pattern: we adapt upward relentlessly, which is why earning more rarely solves what we think it will solve. Financial wellness requires addressing the adaptation cycle, not just increasing the input.

The Radical Case for Enough

Modern culture hates the word enough. Enough suggests limits. Enough implies satisfaction. Enough does not generate clicks. Nobody becomes an influencer by saying: I make a decent living, own a used Honda, and sleep eight hours.

But enough deserves better public relations. Enough means enough savings, enough income, enough security, enough freedom, enough peace. Not endless accumulation. Not infinite optimization. Enough is clarity. And clarity, it turns out, is remarkably good for mental health.

Ancient philosophers discussed this relentlessly. The Stoics called it sufficiency. Epicurus argued that the greatest wealth was not wanting more than you had. Grandparents understood it intuitively. Then somehow we decided fulfillment required becoming our own private equity firms, monetizing every skill and relationship we possess.

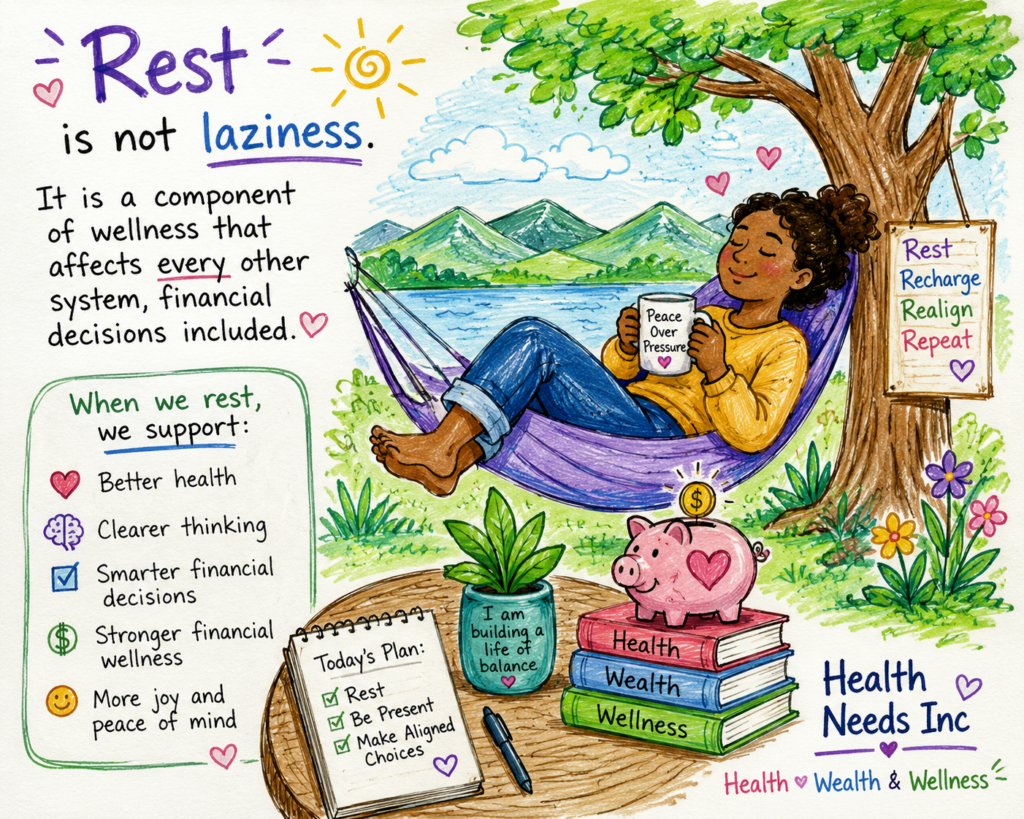

Not every dream requires scaling. Not every hobby requires a revenue model. Not every spare hour needs to justify its existence economically. The side hustle is not evil, but it becomes a problem when it stops being optional. Research on stress recovery consistently shows that unstructured time, the kind with no productivity attached, is essential for both cognitive restoration and emotional regulation. You cannot optimize your way out of needing it.

Financial Wellness Starts With Cash Flow

Fancy investment strategies are entertaining. Cash flow is reality. No amount of cryptocurrency debate can compensate for spending more than you earn. Financial wellness starts with boring fundamentals.

Income and Expenses: The Foundation

Before any other financial wellness conversation is worth having, you need to know where your money comes from and where it goes. Most people have a vague sense of both. A precise accounting of each, even for thirty days, tends to produce revelations. The problem with not tracking spending is that the spending you are most in denial about is always the spending that matters most.

Savings: Pay Yourself First

Automated savings, moved before you have a chance to spend, is the single most effective behavioral finance tool available. It requires no discipline in the moment because the decision has already been made. Research on automatic enrollment in retirement plans has demonstrated that the default option exerts enormous influence on behavior. Set the default toward saving and let inertia work for you instead of against you.

Emergency Funds: Anti-Anxiety Accounts

An emergency fund is typically described as a financial tool. It is equally a psychological one. Three to six months of essential expenses sitting in a savings account buys something invisible: calm. The transmission fails. The dog needs surgery. The refrigerator dies. Without savings, every surprise is a crisis. With savings, an inconvenience replaces a catastrophe. That is a massive difference in how you move through the world. Emergency funds lower cortisol as surely as meditation does, without requiring a meditation practice.

Debt: Mathematics and Emotion Together

Personal finance books portray debt as purely numerical. But humans are not spreadsheets. Debt carries shame, fear, regret, and sometimes genuine trauma. Many people entered adulthood with little financial education, rising housing costs, healthcare expenses that resemble ransom notes, and college tuition that approaches the GDP of small nations. Progress matters more than perfection. Financial healing is still healing, even if nobody is making inspirational reels about paying off a credit card balance.

Protection: The Insurance Nobody Wants to Think About

Appropriate insurance, health, disability, and liability, is not a pessimistic purchase. It is what separates a setback from a financial catastrophe. A single major medical event without adequate coverage can undo a decade of careful saving. The boring infrastructure of financial wellness matters more than most people want to admit until the moment it matters enormously.

Six Practical Steps Toward Financial Wellness

Complexity is overrated. A mediocre plan followed for twenty years defeats a brilliant plan abandoned after three weeks. Here is the boring version that actually works.

1. Track Spending for One Month

Not to judge yourself. Just to know. Use a spreadsheet, a free app, or a notebook. The goal is accuracy, not performance. What you find will surprise you, and the surprise itself is the beginning of agency.

2. Automate Savings Before You Can Spend It

Set up an automatic transfer to a savings account on payday. Start with whatever you can manage, even fifty dollars. The amount matters less initially than the habit. Increase it by one percent per year and compound will do more work than you expect.

3. Build a Three-Month Emergency Fund First

Before investing, before paying off low-interest debt aggressively, build a cash buffer. The psychological value of not having to panic over unexpected expenses changes how you make every other financial decision. Calm people make better choices than panicked people. This is not a controversial claim.

4. Address High-Interest Debt With Intention

Credit card debt at 22% interest is a guaranteed 22% return on every dollar you pay down. No investment reliably beats that. Address it systematically, either by targeting the highest interest rate first (mathematically optimal) or the smallest balance first (psychologically effective, because momentum matters). The right method is the one you will actually follow.

5. Invest Consistently and Boringly

A low-cost index fund held for thirty years will outperform most actively managed portfolios. This is one of the most replicated findings in all of finance. Contribute regularly. Do not time the market. Do not chase trends. Let compounding do its quiet, unhurried work. The retirement planning myths that most people believe almost always involve some version of needing to be smarter or faster than the market. You do not.

6. Define Your Enough Number

What would it cost, per month, to live a life you genuinely liked? Not the aspirational life from a magazine, the actual one. That number, reached and maintained, is the goal. It does not require a lifestyle influencer’s income. It requires clarity about what actually matters to you, which is considerably harder to acquire and considerably more valuable.

Time Is Part of the Financial Wellness Equation

People talk about money as though it exists separately from life. But money and time are inseparable. More money with no time can feel miserable. More time with constant financial panic feels equally bad. The goal is not to maximize one at the expense of the other. The goal is balance, the kind that allows for both security and genuine rest.

This may sound almost heretical, but rest matters. Not because it makes you more productive. Not because naps improve quarterly output. Rest matters because you are a human being, and that should be sufficient justification. Yet modern culture insists that everything justify itself economically. Sleep becomes a productivity hack. Meditation becomes performance enhancement. Even relaxation must apparently submit receipts.

A Sunday afternoon nap can simply be a nap. No branding required. Sleep quality is one of the most consistent predictors of both physical and cognitive health, and it is categorically incompatible with the anxiety that comes from financial systems built entirely around perpetual motion.

Financial wellness is not another mountain to climb. Maybe it is the absence of constant climbing. Maybe it means having enough money, enough stability, enough margin, enough peace. Life is short. Strangely short. Nobody remembers how many productivity apps you mastered or how many side hustles occupied your weekends. They remember the conversations. The meals. The summer evenings. The moments that stubbornly refused to become content.

Money matters because life matters. Not the other way around.

Final Thoughts

Financial wellness without hustle culture is not laziness, not lack of ambition, and not giving up. It is deciding that your bank account should support your life rather than consume it.

The irony is that the boring path, track spending, automate savings, build an emergency fund, invest consistently, define your enough, produces better outcomes than almost everything the financial content industry sells. It just does not make a good thirty-second video.

The single most important thing to take from this: financial wellness is a state, not a destination on an infinite leaderboard. It is the state of having enough margin to make choices. Everything else, the spreadsheets, the apps, the side hustles, the investment strategies, is either in service of that state or a distraction from it.

Start with one concrete thing: open a savings account if you do not have one, set up a fifty-dollar automatic transfer, or write down what you spent last month. One boring step in the right direction is worth more than a hundred brilliant plans you will never execute.

Then, with the finances tended to, go outside. The sunsets are still free.

Frequently Asked Questions About Financial Wellness

Financial wellness is the state of having enough stability, margin, and control over your finances to meet obligations, absorb unexpected expenses, and make choices that let you enjoy your life. Wealth is the accumulation of assets. The two often overlap, but they are not the same thing. A person can have significant assets and still experience severe financial anxiety. Conversely, someone with modest income but a solid emergency fund, manageable debt, and clear priorities can have excellent financial wellness. The Consumer Financial Protection Bureau defines financial well-being around control, security, and freedom of choice, not net worth.

The evidence is mixed and context-dependent. Additional income from a side hustle can genuinely accelerate savings and reduce debt if the income is directed intentionally rather than absorbed by lifestyle expansion. However, hustle culture as a philosophy, the idea that productivity is morally superior to rest and that all available hours should be monetized, is associated with elevated chronic stress, sleep disruption, and burnout. These have direct financial consequences: impaired decision-making, reduced earning capacity over time, and increased healthcare costs. Working more hours is not the same as building financial wellness. The direction of the effort matters as much as the quantity of it.

The standard recommendation from most financial planners is three to six months of essential living expenses, meaning the minimum you need to cover housing, food, utilities, transportation, and basic insurance. For people with variable income, freelance or commission-based work, or jobs in volatile industries, six to twelve months provides considerably more stability. The key is that the fund should be liquid, meaning in a savings account you can access immediately, and mentally reserved for genuine emergencies rather than irregular planned expenses. Starting small and building incrementally is far better than waiting until you can fund it all at once.

This is the hedonic adaptation problem. Psychologists have documented that humans adapt rapidly to improved circumstances: the new salary becomes the baseline, lifestyle expands to match it, and the stress returns to previous levels. This is sometimes called the hedonic treadmill. Additionally, higher income often comes with higher expectations, greater responsibility, longer hours, and higher social comparison stakes. Research suggests the relationship between income and subjective well-being is real but nonlinear. The largest gains come from moving out of genuine financial hardship. Beyond a moderate baseline, the incremental happiness gains from each additional dollar diminish sharply, particularly if those dollars come at the cost of time, autonomy, or sleep.

Track your actual spending for thirty days. Not to judge yourself, not to build a perfect budget, just to know the truth. Most people significantly underestimate their discretionary spending and have only a vague sense of where their money actually goes. Clarity precedes change. Once you know what is actually happening, you can make one concrete adjustment: automate a savings transfer, pay down one card, or cancel one subscription you do not use. Small, maintained improvements compound over time in the same way investments do. The goal is not a perfect financial plan. It is a functional one you will actually follow.

Yes, under specific conditions. A side hustle makes sense when it addresses a genuine financial gap, when the income is directed toward a concrete goal such as an emergency fund or debt payoff, and when it does not systematically erode sleep, health, or primary relationships. The problem is not side hustles themselves. The problem is when side hustles become mandatory rather than optional, when rest is reframed as wasted productivity, and when the additional income simply funds lifestyle inflation rather than building financial margin. Evaluate any side hustle against this question: does this move me closer to financial wellness, or does it just keep me busier?

Financial stress is one of the most common and consequential forms of chronic stress. It is associated with elevated cortisol levels, disrupted sleep, increased anxiety and depression risk, impaired cognitive function, and higher rates of cardiovascular disease. A report from the American Psychological Association has consistently found that money ranks among the top sources of stress for Americans across income levels. Financial stress is not simply a problem for people with low incomes. It affects anyone whose financial situation lacks the margin to absorb shocks or make free choices. This is why financial wellness is considered an integral dimension of overall wellness, not a separate category.