This article is for educational and informational purposes only and is not financial advice. Consult a qualified financial professional before making changes to your financial strategy.

Financial Wellness: Building a Healthier Relationship With Money

What financial wellness actually means, why chronic money stress is a health problem, and the four unglamorous foundations that actually work.

What Is Financial Wellness, and Why Does It Belong in a Health Conversation?

What is financial wellness?

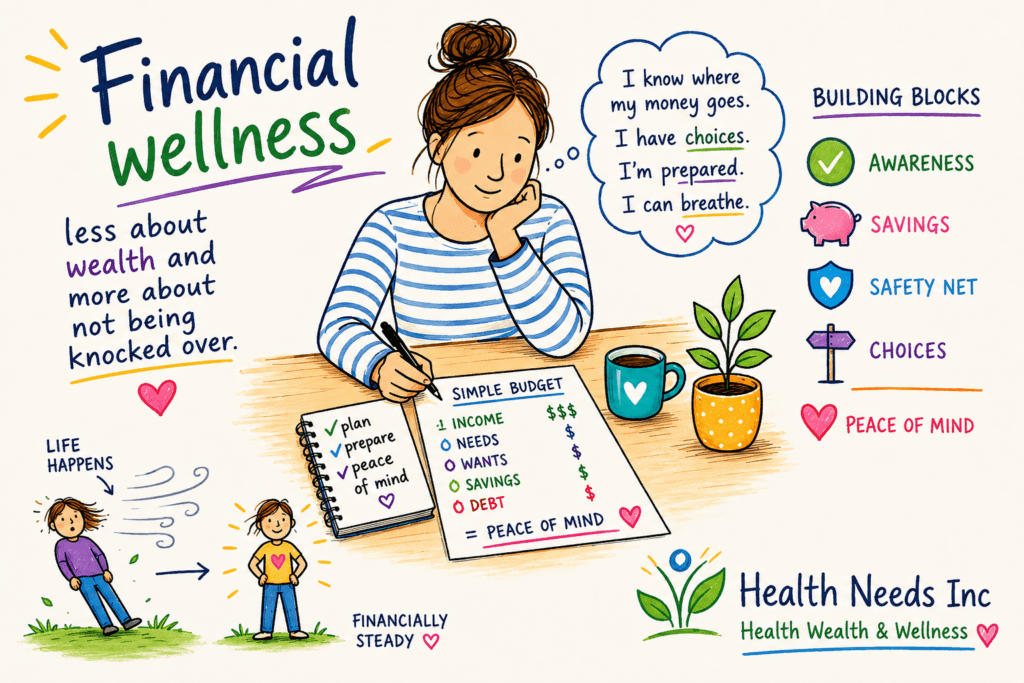

Financial wellness is the ability to meet your current financial needs while preparing for the future, without chronic stress eroding your health in the process. According to the Consumer Financial Protection Bureau, it encompasses four elements: control over day-to-day finances, capacity to absorb a financial shock, progress toward financial goals, and the freedom to make choices. It is not a net worth number. It is a functional state.

Key Takeaways

Financial wellness is defined by stability and low stress, not by wealth. A person earning $50K with a solid emergency fund may be more financially well than a high earner living paycheck to paycheck.

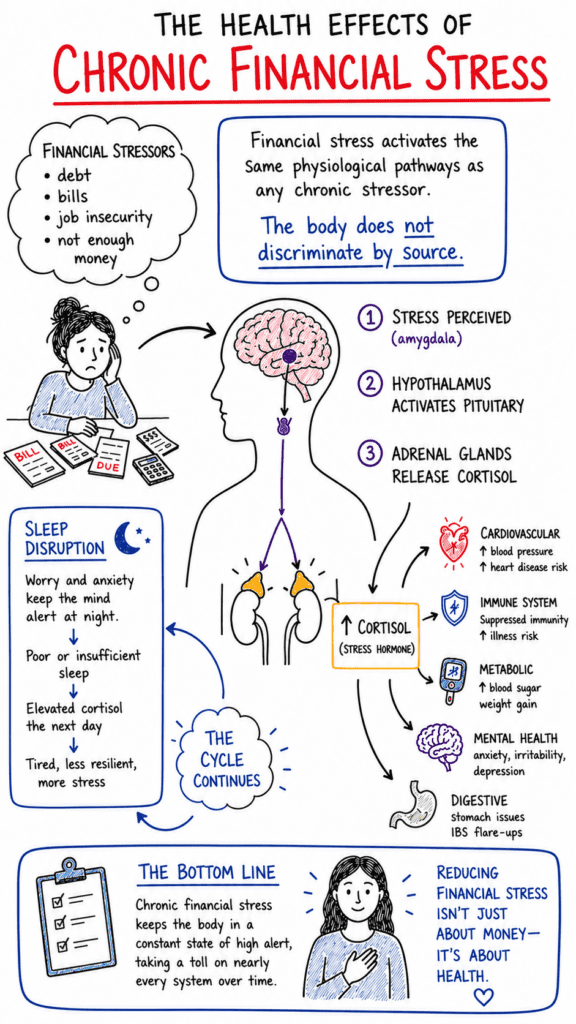

Financial stress activates the same physiological pathways as other chronic stressors, contributing to anxiety, sleep disruption, and relationship conflict.

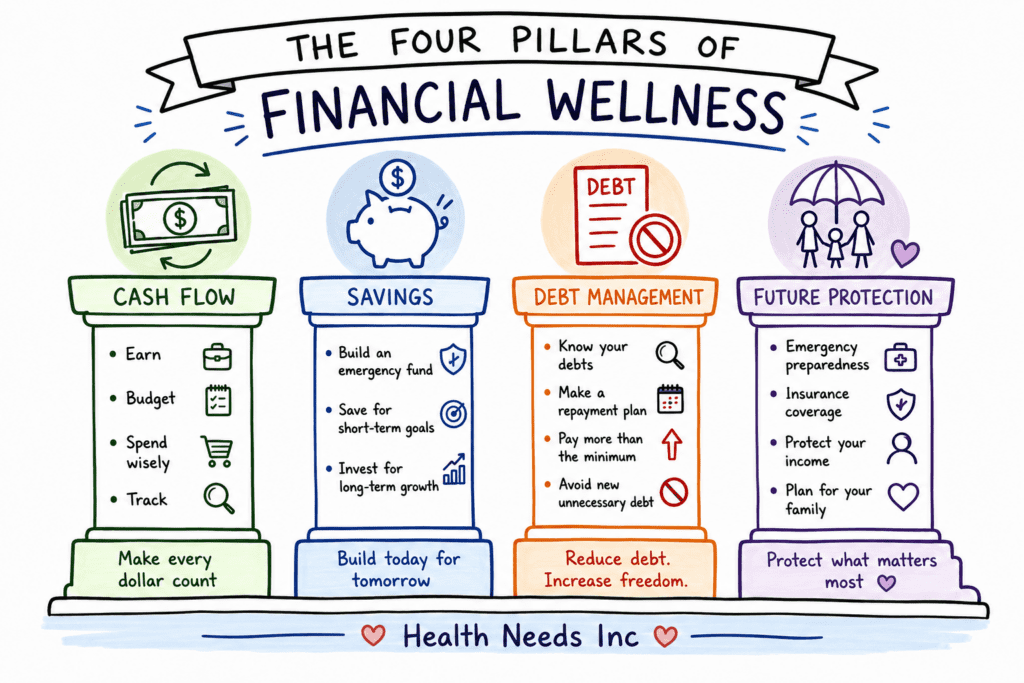

The four foundations of financial wellness are cash flow awareness, emergency savings, debt management, and future protection. None of them require wealth to start.

Small, consistent habits reliably outperform dramatic financial overhauls. Boring works.

Progress, not perfection, is the operative standard. Everyone makes financial mistakes. Everyone.

The real goal of financial wellness is resilience: the ability to absorb setbacks without catastrophic outcomes.

Financial Wellness Belongs in the Health Conversation

The bills arrive. Markets bounce around like caffeinated squirrels. Retirement lurks in the distance. Somewhere, a twenty-three-year-old influencer is explaining how anyone can become rich before lunch. Financial wellness is the discipline that sits in the middle of all that noise and quietly refuses to be impressed by any of it.

It is not becoming a millionaire. It is not retiring at forty-two while posting photos from a beach in Bali. It certainly is not buying a course from someone standing beside a rented Lamborghini.

Researchers have consistently found that financial strain affects emotional health, sleep quality, relationships, and physical well-being. Money problems rarely stay in their lane. They wander into every room of the house, which is precisely why financial wellness deserves a place alongside physical, emotional, and social wellness in any serious discussion of health.

The wellness industry often sells optimization. Financial wellness is something quieter. It is the ability to sleep without wondering if a surprise expense will wreck your life. Understanding what that state actually requires, and how to build it without heroic effort, is what this article is for.

What Financial Wellness Actually Is

The Consumer Financial Protection Bureau defines financial well-being as a state in which a person can fully meet current and ongoing financial obligations, feel secure in their financial future, and make choices that allow them to enjoy life. Note what is not in that definition: a specific income level, a net worth target, or a retirement account balance.

That matters. A person earning $50,000 a year with three months of expenses saved and zero high-interest debt may be more financially well than someone earning $200,000 who has assembled an impressive lifestyle they cannot afford to pause for a single month. The metric is functional stability, not wealth accumulation.

Financial wellness also sits as one of the eight recognized dimensions of wellness, alongside physical, emotional, social, occupational, intellectual, environmental, and spiritual health. Treating it as a silo misses the point. Financial instability radiates outward into every other dimension.

The Four Foundations of Financial Wellness

Most financial health rests on four surprisingly unexciting pillars. There is no fifth secret. There is no hack. The boring architecture is the point.

1. Cash Flow Awareness

Money coming in. Money going out. That is the whole magic trick. You do not need complicated spreadsheets worthy of a NASA launch. You need enough awareness to know where your money disappears each month. Many people discover their budget has been quietly assassinated by subscriptions they forgot existed and takeout meals that seemed reasonable one receipt at a time.

2. Emergency Savings

Life enjoys surprises, usually the expensive variety. Cars break. Furnaces revolt. Teeth occasionally stage mutinies. Emergency savings are less about earning interest and more about buying peace of mind. Even a modest cushion, the standard target is three to six months of expenses, can prevent minor setbacks from becoming financial catastrophes. The purpose is not perfection. It is resilience.

3. Debt Management

Debt itself is not evil. Mortgages helped millions of people buy homes. Student loans have opened doors that were otherwise sealed shut. High-interest debt, however, behaves like an unwelcome houseguest. It eats your food, raises your blood pressure, and refuses to leave. Financial wellness means creating a strategy to manage debt rather than pretending it does not exist. Ignoring debt works about as well as ignoring smoke coming from the basement.

4. Future Protection

Eventually tomorrow becomes today. Retirement planning, insurance coverage, estate planning, and long-term investing are all ways of protecting the future version of yourself. The older you become, the more you realize that your greatest act of financial kindness may be helping the person you will be twenty years from now. Future You deserves some consideration. Current You has already made enough questionable decisions.

Why Financial Wellness Is a Health Issue

The connection between financial stress and physical health is not metaphorical. Research from the American Psychological Association consistently shows money as a leading source of chronic stress in American adults, outranking work, personal relationships, and health concerns in many survey years. Chronic stress, regardless of its source, activates the HPA axis, floods the body with cortisol, and creates downstream effects on sleep, immune function, and cardiovascular health.

Financial instability also correlates with higher rates of anxiety and depression. A 2020 review in Social Science and Medicine found significant associations between debt and poor mental health outcomes, with high-interest consumer debt showing the strongest links. The mechanism appears to be less about the debt itself and more about the perceived inability to escape it.

The overlap with chronic cortisol elevation is worth noting specifically. Financial uncertainty triggers the same threat-detection machinery that evolution built for physical danger. The brain does not meaningfully distinguish between a charging predator and a maxed-out credit card. Stress hormones arrive either way, and their long-term presence is the problem.

The Perfection Problem in Financial Wellness

This is where most people quietly give up. They assume everyone else has their finances under control, an illusion made possible by social media, where nobody posts pictures of arguing with their spouse about the electric bill, and nobody uploads videos titled “Just spent thirty minutes searching for a coupon code while questioning every life choice.”

The comparison trap is particularly vicious in personal finance because the successful outcomes are visible (new car, vacation photos, early retirement announcements) and the struggle is largely invisible. The result is a persistent feeling that you are behind a race everyone else is winning.

The evidence does not support that narrative. According to the Federal Reserve’s annual Report on the Economic Well-Being of U.S. Households, a substantial portion of American adults cannot cover a $400 emergency expense without borrowing. The average household carries significant credit card debt. The crisis is common. The silence around it is what creates the illusion of rarity.

Financial wellness does not require never making mistakes. Everyone makes mistakes. The goal is progress, not perfection. Good enough beats perfect every single time, because perfect is a reason to never start.

Money, Stress, and Your Nervous System

Financial stress has been linked to anxiety, depression, sleep disturbances, and relationship strain. The physiological pathway is well documented: uncertainty activates the sympathetic nervous system, which is useful for short-term threats and corrosive over long-term exposures. Chronic money worries keep the system in a low-grade alert state, which is exhausting in a way that is difficult to attribute to any single cause.

Improving financial wellness often produces benefits that extend well beyond the bank account. People frequently report sleeping better, arguing less with partners, and feeling more optimistic about the future once a basic financial floor is established. Not because money solves every problem, it does not, but because uncertainty is itself exhausting. Removing uncertainty has a measurable calming effect on the nervous system, even when the total dollars involved are modest.

This is also why the psychological research on financial wellness tends to emphasize perceived control over objective wealth. Feeling in control of your finances, even at a modest income level, correlates more strongly with positive well-being outcomes than a high income with low perceived control. The floor matters more than the ceiling.

Financial Wellness Habits That Actually Work

Financial wellness does not require heroic acts. Small habits consistently applied outperform dramatic overhauls every time. The research on behavior change supports this: large sweeping changes tend to collapse under their own ambition. Small, sustainable systems tend to compound.

1. Track Spending Without Obsession

Awareness is the intervention. You do not need to categorize every transaction to four decimal places. A monthly review of major categories, food, housing, subscriptions, transportation, takes about twenty minutes and produces a disproportionate amount of useful information. Most people find at least one or two recurring charges they had forgotten about entirely.

2. Build Emergency Savings Gradually

Starting with $500 is more useful than waiting until you can save $5,000 at once. The goal is to create a buffer between you and the next surprise. Automate the transfer if possible. The best savings strategy is one that requires no willpower to maintain.

3. Pay Down High-Interest Debt Strategically

The two most common debt payoff strategies are the avalanche (highest interest rate first, mathematically optimal) and the snowball (smallest balance first, psychologically effective). Research published in the Journal of Consumer Research suggests the snowball method works better for most people precisely because the early wins sustain motivation. Pick the one you will actually use.

4. Increase Retirement Contributions Over Time

Contributing even 1% of income to a retirement account, and increasing that percentage by 1% each year, produces substantial long-term results without requiring dramatic lifestyle changes. The most common retirement myths involve believing you need to wait until you can contribute large amounts. The compounding math works better when you start small and early.

5. Review Insurance Coverage Annually

Insurance is the least exciting topic in personal finance and also one of the most consequential. A single gap in health, disability, or property coverage can undo years of financial progress in one event. An annual review takes an hour and often costs nothing except the mild discomfort of reading your policy documents.

6. Ask for Professional Advice When the Stakes Are High

A fee-only financial advisor (one who earns no commissions) can be useful at key decision points: major life transitions, approaching retirement, or any situation complex enough to have meaningful downside risk. This is not an ongoing subscription. It is targeted expertise when the cost of getting it wrong is high.

A More Human Definition of Financial Wellness

Perhaps financial wellness has less to do with accumulating endless money and more to do with having enough. Enough security. Enough flexibility. Enough peace of mind. Enough freedom to make choices based on values rather than panic.

The wellness industry sells optimization relentlessly. Optimize your sleep. Optimize your nutrition. Optimize your portfolio. The implicit message is that current you is a suboptimal version of the person you could become, and the solution is always just one more purchase away. Financial wellness, properly understood, is a quiet counterargument to all of that.

It is the ability to sleep without wondering if a surprise expense will wreck your life. It is knowing that setbacks happen and believing you have the capacity to handle them. It is understanding that money is a tool, not an identity, and that the goal of financial health is the same as the goal of physical health: not perfection, but durability.

Final Thoughts

Financial wellness sits at the intersection of practical behavior and psychological health in ways that the personal finance industry rarely acknowledges and the wellness industry rarely addresses. It is too numbers-adjacent for the mindfulness crowd and too feelings-adjacent for the spreadsheet crowd.

That gap is part of why so many people feel stuck. The math is manageable. The psychology is the hard part.

The evidence, for what it is worth, points in a consistent direction: the most effective path to financial wellness is not a dramatic overhaul or a six-figure income. It is a modest emergency fund, a clear picture of cash flow, a strategy for high-interest debt, and some protection for the future. Everything else is optimization on top of that foundation.

Start with the smallest step that feels real. Track one month of spending. Transfer $25 to a dedicated savings account. Call your insurance agent. None of these are inspiring acts. That is precisely the point.

Becoming difficult to knock over is not glamorous. It is, however, the thing that actually works.

Frequently Asked Questions About Financial Wellness

Financial wellness refers to a functional state of financial health characterized by stability, low stress, and a sense of control, not a specific income level or net worth. The Consumer Financial Protection Bureau defines it as having the capacity to meet current obligations, absorb financial shocks, make progress toward goals, and enjoy some financial freedom of choice. A person can be financially well on a modest income and financially unwell on a high income, depending entirely on the gap between resources and obligations.

Financial stress activates the same neurological and hormonal stress pathways as other chronic stressors, including elevated cortisol, disrupted sleep, and heightened anxiety. Research consistently links financial strain to higher rates of depression, cardiovascular problems, and relationship conflict. The mechanism is not primarily about the money itself but about the chronic uncertainty and perceived lack of control that financial instability creates. Reducing that uncertainty, even modestly, produces measurable improvements in well-being.

The evidence-based foundations are: (1) cash flow awareness, knowing where your money goes each month; (2) a starter emergency fund of at least $500 to $1,000, growing toward three to six months of expenses; (3) a strategy for paying down high-interest debt; and (4) some form of future protection, including retirement savings and adequate insurance coverage. These four elements do not require high income to begin. They require consistency applied to whatever resources are currently available.

The standard recommendation from most financial planners is three to six months of essential living expenses. However, the most important threshold is the first one: having any buffer at all. Research and behavioral finance both suggest that a $500 to $1,000 emergency fund eliminates a large proportion of minor financial emergencies that would otherwise require credit card debt. Build toward three months first, then extend from there. The precise amount matters less than having something, and having it in a dedicated account that is not easily raided for non-emergencies.

Yes. Financial wellness is one of the eight recognized dimensions of wellness, alongside physical, emotional, social, occupational, intellectual, environmental, and spiritual health. The dimensions interact: financial instability creates chronic stress that degrades physical and emotional health, while poor physical health can create financial instability through medical costs and reduced earning capacity. Treating financial health as a separate domain from general wellness misses the feedback loops that connect them.

The research suggests yes, with an important nuance: it is perceived control and reduced uncertainty rather than absolute wealth that drives most of the mental health benefit. Studies show that people who feel in control of their financial situation report significantly better psychological well-being than people with objectively higher incomes but low perceived control. Building even a modest emergency fund and a clear picture of cash flow can produce improvements in anxiety and sleep quality that are disproportionate to the dollar amounts involved.