This article is for educational and informational purposes only and is not financial or legal advice. Your situation may involve taxes, debt, health, family obligations, or legal issues that deserve a qualified professional’s attention.

Financial Wellness: A Practical Guide for Adults Tired of Pretending Money Is Just Mindset

What financial wellness actually means, why money stress feels so physical, and how to build real stability without joining a money cult.

What Is Financial Wellness, and Why Does It Matter?

What does financial wellness actually mean?

Financial wellness is the condition of having enough stability, control, and flexibility in your financial life to meet current needs, absorb surprises, and make future choices. The Consumer Financial Protection Bureau defines financial well-being as the degree to which your financial situation and choices provide both security and freedom of choice, in the present and into the future.

Key Takeaways

Financial wellness is not about income level. It is about resilience: can you handle your needs, absorb a surprise, and make choices from information rather than panic?

Money stress is not just a mindset problem. It shows up in your body, your sleep, your relationships, and your ability to open mail without dread.

The four building blocks of financial wellness are cash flow visibility, an emergency cushion, a debt strategy, and future protection.

A starter emergency fund of $250 to $500 can prevent a flat tire from becoming a payday loan spiral. Start small. The number is not the point. The habit is.

The best debt payoff strategy is the one you can continue after a bad week. Mathematically optimal plans mean nothing if they collapse under real life.

Knowing when to ask for qualified help is a sign of financial maturity, not defeat. The internet is not always enough.

The Problem With Most Financial Wellness Advice

Spend less. Hustle more. Manifest abundance. Stop buying coffee. Start investing yesterday. Build seven income streams before breakfast. Somewhere, a man with a rented Lamborghini wants to teach you discipline for $997. Financial wellness is none of that.

It is not about becoming a money monk. It is not about pretending compound interest will soothe every human fear. And it is definitely not about blaming people for living inside an economy where rent, groceries, healthcare, childcare, and interest rates have all apparently joined a villainous barbershop quartet.

The Consumer Financial Protection Bureau describes financial well-being as the degree to which your financial situation and choices provide security and freedom of choice. That is a useful definition precisely because it leaves room for real life. Financial wellness is not just how much money you have. It is whether your money gives you breathing room or steals your sleep.

This guide is not a sermon. It is not a sales pitch. It is a map of four practical areas, a set of specific starting moves, and an honest account of what financial wellness actually is, and what it is definitely not.

What Financial Wellness Actually Means

Financial wellness is often marketed as a vibe. In reality, it is more like plumbing. You notice it most when something is leaking.

At its core, financial wellness means you can handle your present needs, absorb some surprises, and make future choices without every decision feeling like a trapdoor. The Federal Reserve’s annual household survey found that 73% of adults reported doing okay or living comfortably financially near the end of 2024, while 27% were either just getting by or finding it difficult to get by. That is not a disaster picture. But it is also not a kingdom of security.

Financial wellness includes paying regular bills without constant crisis, understanding where your money goes, having some emergency cushion, managing debt instead of being managed by it, planning for future needs, and knowing when to ask for help. It does not mean you are rich. Plenty of high-income households are financially brittle. Plenty of modest-income households are careful, stable, and still one medical bill away from chaos. Financial wellness is not a moral ranking system. It is a condition of resilience.

Why Money Stress Feels So Physical

Money stress does not stay politely inside a banking app. It shows up in your jaw. Your sleep. Your patience. Your relationships. Your ability to open mail without feeling like you are defusing a bomb.

That is because money is not just arithmetic. It is safety, status, time, healthcare, housing, dignity, options, and the ability to say no. When those feel threatened, the body pays attention. The nervous system does not distinguish between a charging predator and a threatening overdraft notice. Both arrive as danger. If you want to understand what chronic stress does to your body beyond the financial layer, that is a separate and connected story.

This is where a lot of wellness advice becomes insulting. Financial wellness sits at the intersection of nervous system and invoice. It does not ask you to meditate your way out of math. It asks you to make the math visible enough that fear stops multiplying in the dark. That is a meaningful distinction, and it is one worth holding onto when the advice starts sounding like victim-blaming with better typography.

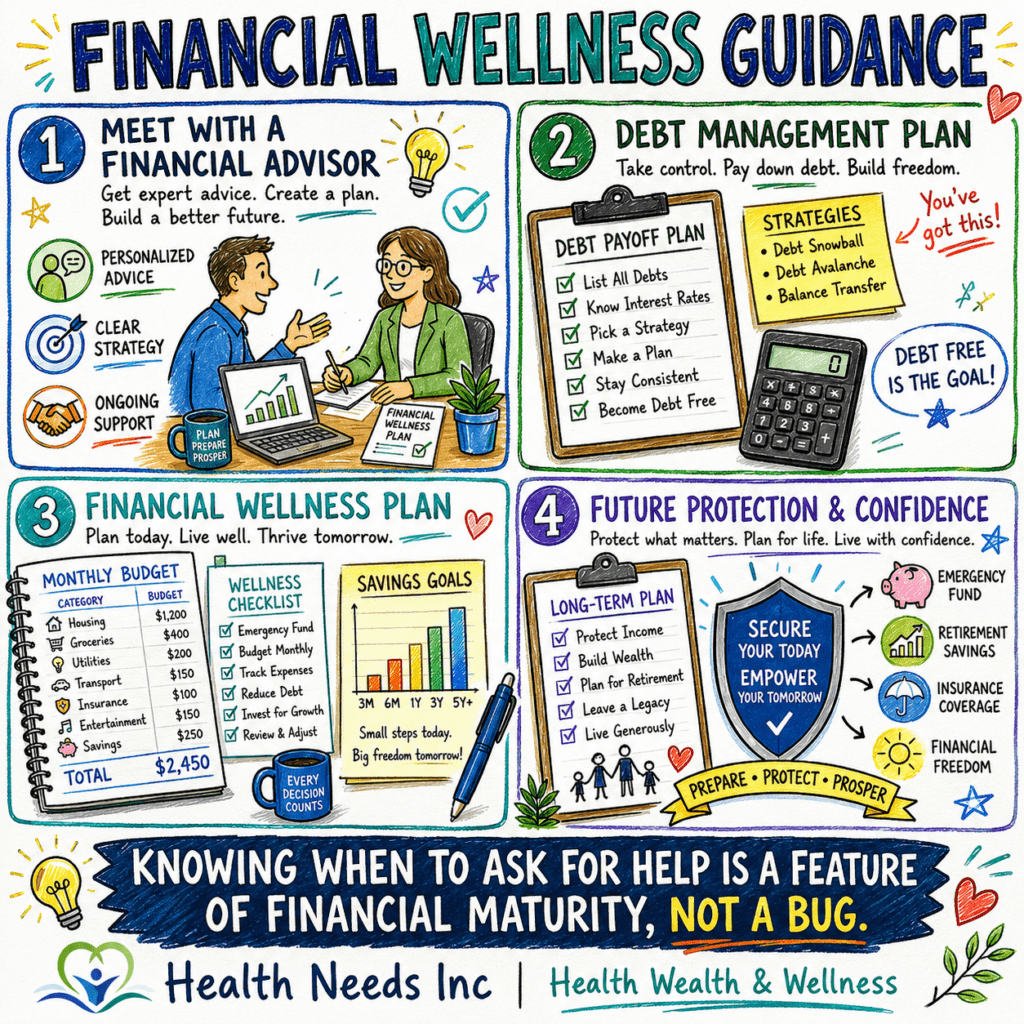

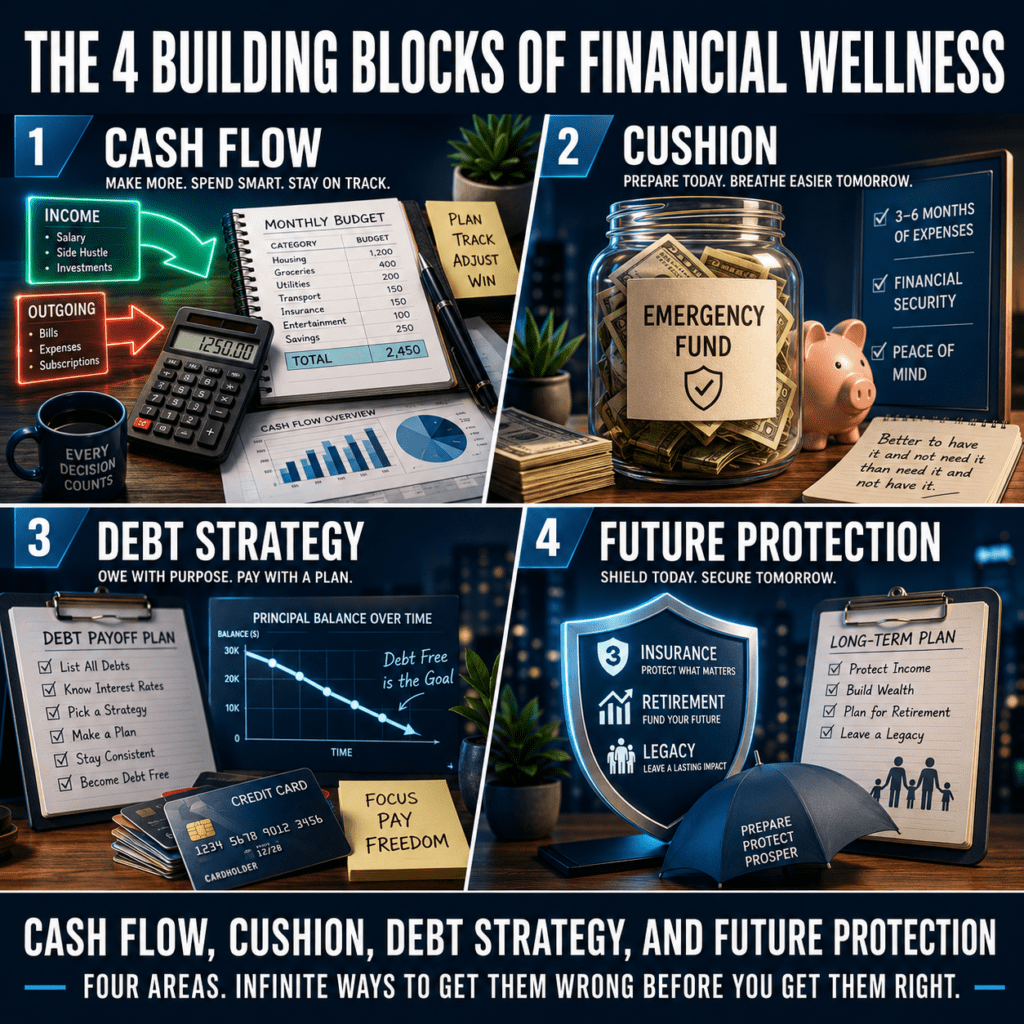

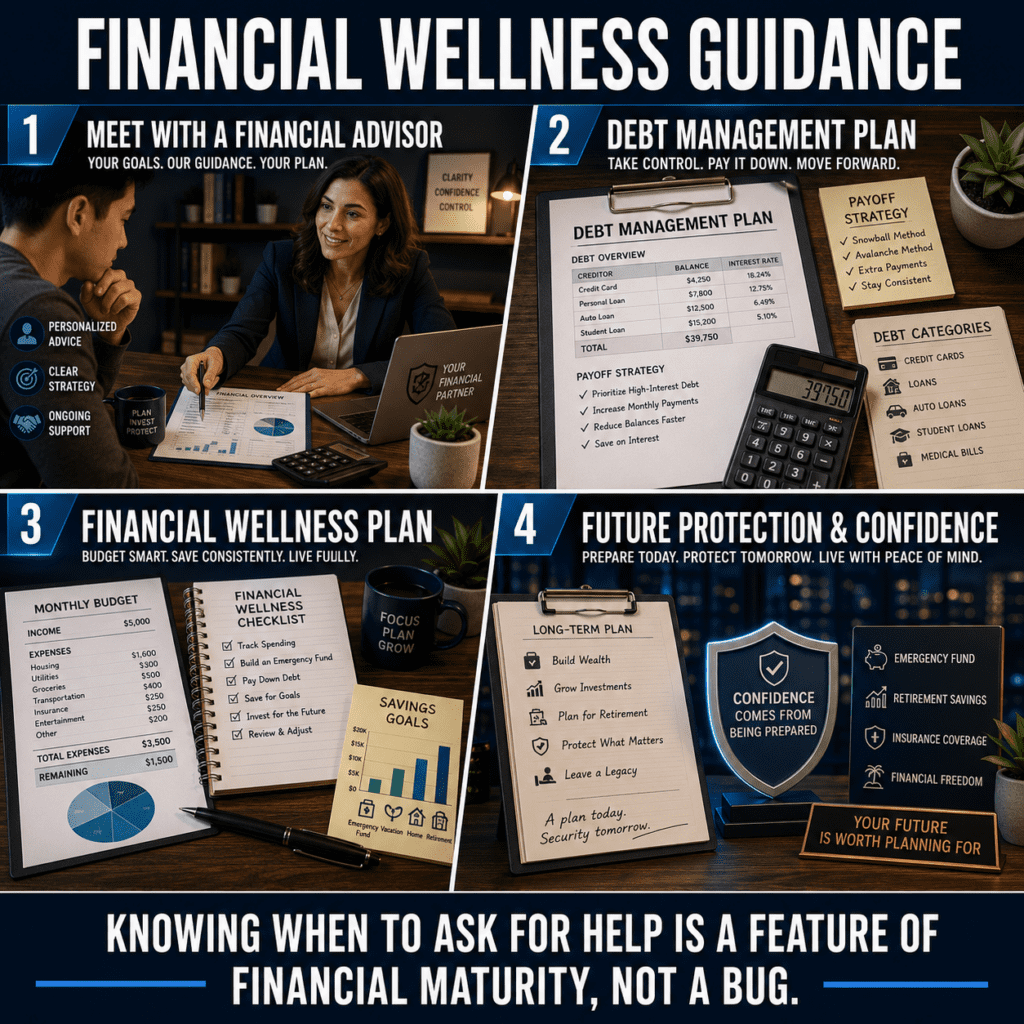

The Four Building Blocks of Financial Wellness

Financial wellness is easier to build when you stop treating it as one enormous problem and start treating it as four smaller ones. Here is how the structure works.

1. Cash Flow

Cash flow is what comes in and what goes out. This sounds obvious, which is exactly how it tricks people. Many financial problems begin as vague fog. You know money is disappearing. You suspect groceries are involved. There may be subscriptions. The first step is not judgment. It is visibility. Look at one month of income and expenses. Sort spending into categories: housing, food, transportation, insurance, debt, savings, subscriptions, health, family obligations, and miscellaneous. The point is not perfection. The point is to stop guessing.

2. Cushion

A cushion is money that stands between you and panic. The classic advice is to save three to six months of expenses. Fine. But for many people, that number is so large it becomes useless as a starting point. A better entry might be $250, $500, or one week of essential expenses. Small buffers matter. They can prevent a flat tire from becoming a payday loan, a missed bill, or a credit card spiral. The Federal Reserve’s household surveys regularly examine emergency expense coverage precisely because financial fragility often shows up not in annual income but in how people absorb surprise costs.

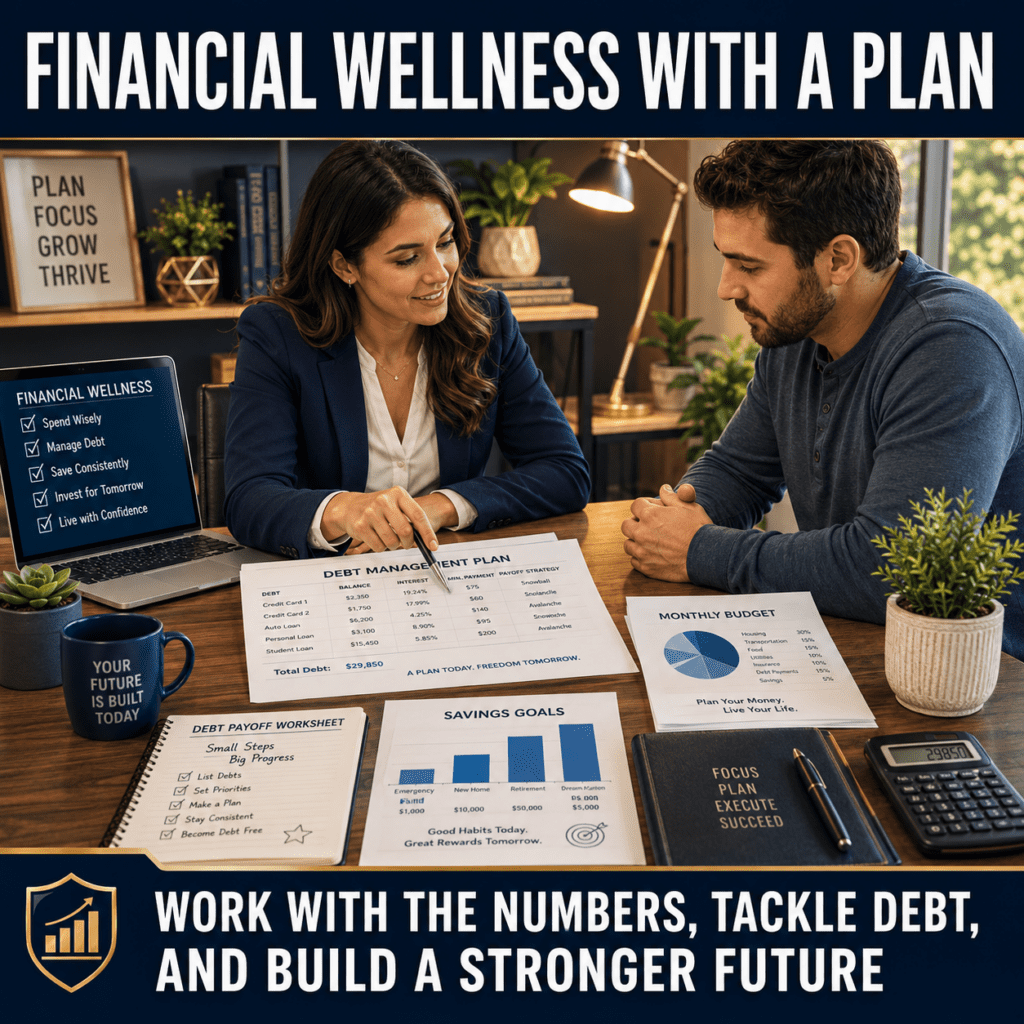

3. Debt

Debt is not automatically evil. Used carefully, it can fund education, housing, transportation, or necessary flexibility. But high-interest consumer debt can become financial kudzu. It grows over everything. The first step is to list all debts: balances, interest rates, minimum payments, and due dates. Then choose a strategy. The avalanche method targets the highest-interest debt first: mathematically elegant, very spreadsheet-approved. The snowball method targets the smallest balance first: psychologically satisfying, because sometimes momentum beats purity. The best debt strategy is the one you can continue after a bad week.

4. Future Protection

Future planning is the least glamorous part of financial wellness, which is probably why it keeps getting skipped. It includes retirement savings, insurance, estate documents, beneficiary updates, tax planning, and a plan for what happens if your income stops. The FINRA National Financial Capability Study tracks financial behaviors, attitudes, and knowledge because financial capability is not one skill. It is a cluster of habits, tools, knowledge, and circumstances. Future protection is the part of that cluster most people build last and need earliest.

How to Improve Financial Wellness Without Joining a Money Cult

Start small. Start boring. Start where you are.

1. Take One Honest Snapshot

Gather your income, regular expenses, debts, savings, and upcoming obligations. A one-page snapshot is enough. You want to know: monthly take-home income, essential expenses, debt minimums, savings balance, major upcoming costs, and one or two spending leaks. That is it. No shame ceremony required. You cannot fix what you refuse to look at, but you also do not need to fix everything in one heroic afternoon.

2. Build a Tiny Emergency Buffer

Before optimizing your entire financial life, create a small buffer. Even $10 or $25 per paycheck matters if it stays untouched. Put it somewhere separate from daily spending. Give it a boring name like “Emergency Fund,” not “Boat Money,” unless you are emotionally prepared to become a person with boat problems.

3. Pick One Debt Move

Do not try to fix every debt at once. Pick one: pay an extra amount toward the highest-interest balance, pay off the smallest balance for momentum, call a lender and ask about hardship options, or consider nonprofit credit counseling. Debt payoff is not a personality test. It is a logistics problem with emotional shrapnel. Stop adding new charges while you stabilize, if you can. That alone changes the trajectory.

4. Automate the Boring Stuff

Automation helps because humans are inconsistent mammals. Automate minimum debt payments to avoid late fees. Automate savings, even if the amount is tiny. Automate retirement contributions if available through work. Boring systems beat heroic intentions every time, and they keep working on days when you are tired, distracted, or busy being a person.

What Financial Wellness Is Not

Financial wellness is not moral purity. You are not bad with money because you bought a coffee. You are not enlightened because you meal-prepped lentils. Most people’s financial lives are shaped by income, costs, family responsibilities, health, geography, debt, luck, policy, and timing. Behavior matters. So do systems. And so do circumstances that no amount of individual discipline can fully override.

Financial wellness is also not buying every product that calls itself empowering. Some tools help. Some are just fees wearing inspirational sneakers. Be especially cautious with high-fee debt settlement programs, payday loans, buy now pay later overuse, meme-stock speculation, crypto promises, insurance products you do not understand, financial coaches with no clear credentials, and anything marketed with the phrase “guaranteed returns.” A good financial tool should make your life clearer, safer, or more efficient. It should not require you to ignore your instincts.

A Practical Financial Wellness Checklist

Use this as a starting point, not a report card. Complete one item at a time if that is what the situation allows.

Foundation Moves

- Review one month of spending and sort into categories

- List all debts with balances and interest rates

- Build a starter emergency fund of $250 to $500

- Set bills to autopay where it is safe to do so

- Cancel unused subscriptions

Stability Moves

- Check your credit report at AnnualCreditReport.com

- Review insurance basics: health, auto, renters or homeowners

- Increase retirement contributions gradually if available

- Keep financial documents in one place

- Ask for qualified help when the stakes are high

When to Talk to a Professional

Consider professional help if you are facing bankruptcy, tax debt, foreclosure, wage garnishment, divorce, major medical bills, inheritance issues, significant investment decisions, retirement planning, or the need for legal documents like wills and powers of attorney.

Financial wellness does not mean doing everything alone. In fact, knowing when the internet is not enough is one of the clearest signs of financial maturity. A good professional should explain options clearly, disclose fees, respect your goals, and avoid pressure tactics. If someone makes you feel stupid, rushed, or dazzled, leave. Confusion is not a business model you need to subsidize.

Resources worth knowing: the National Foundation for Credit Counseling connects people with nonprofit credit counselors. The CFPB’s housing counselor tool helps people facing mortgage trouble. For tax issues, the Taxpayer Advocate Service exists specifically to help people navigate problems with the IRS. These are not exciting resources. They are useful ones.

Final Thoughts

Financial wellness is not a glow-up. It does not arrive after one powerful morning routine or a seminar in a hotel ballroom. It is maintenance. It is plumbing. It is checking the tires before the road trip, and then actually checking them again the next time.

The real goal is quieter than it sounds in most marketing. To know what is happening with your money. To build a little room between yourself and disaster. To make choices from information instead of panic. To stop treating money like either a personal failure or a magical scoreboard that measures your worth as a human being.

Most people will not achieve perfect financial stability. Life does not hold still long enough for that. But most people can achieve something more useful: a little more visibility, a little more cushion, a slightly less terrifying relationship with their inbox. That is where financial wellness actually lives. Not in the aspirational version, but in the real one.

Pick one thing from this article. Do it this week. Then pick another. That is the whole method, and it works better than any $997 webinar. Which, for the record, is not a high bar, but it is still satisfying to clear it.

Frequently Asked Questions About Financial Wellness

Financial wellness means having enough control, stability, and flexibility in your financial life to meet current needs, handle some surprises, and make future choices. The CFPB frames financial well-being around two dimensions: security and freedom of choice, both in the present and looking ahead. It is not a measure of wealth. It is a measure of resilience.

Financial literacy is what you know. Financial wellness is how your money life is actually functioning. You can understand interest rates perfectly and still be stressed, underpaid, overextended, or one emergency away from trouble. Literacy is knowledge. Wellness is the lived condition of your finances. Both matter. They are not the same thing.

The conventional target is three to six months of essential expenses, but that number can feel paralyzing if you are starting from zero. A more useful entry point is $250 to $500 as a starter fund. Even a small buffer reduces dependence on credit cards or high-cost borrowing during minor emergencies. Build from there once the habit is established.

Yes. Financial stress can contribute to sleep problems, anxiety, relationship conflict, and physical tension. It should not be treated as a mindset issue that meditation alone can solve. Money affects real choices around housing, food, healthcare, transportation, and time. Both the nervous system and the budget deserve attention. Addressing one without the other is only half the picture.

No. Some debt is useful or necessary. Mortgages, student loans, and auto financing can all serve legitimate purposes depending on the terms and the situation. The bigger concern is whether the debt is affordable, understandable, and aligned with your goals. High-interest consumer debt deserves special attention because it grows quickly and can overwhelm a budget faster than people expect.

Start with a clear snapshot: income, expenses, debts, savings, and upcoming obligations. A single page is enough. You cannot fix what you refuse to look at, and you do not need to fix everything at once. Visibility comes before optimization. Most people find that simply knowing what is happening reduces at least some of the anxiety that thrives in the fog of not knowing.