This article is for educational and informational purposes only and is not financial or legal advice. Consult a qualified financial professional before making changes to your retirement strategy.

Catch-Up Strategies After 50: Retirement Planning Without Panic

Behind on retirement savings? Here is what the rules actually allow, what order to do things in, and why shame is the worst financial planner you will ever hire.

Catch-Up Strategies After 50: What Actually Works

What are the best catch-up strategies for retirement savings after 50?

Catch-up strategies after 50 work through a combination of higher IRS contribution limits, debt reduction, employer match capture, and Social Security timing. In 2026, workers 50 and older can contribute up to $32,500 to eligible workplace plans, with a higher $35,750 limit for those turning ages 60 to 63.

The most effective approach sequences these moves deliberately: capture the employer match first, eliminate high-interest debt second, and increase contributions progressively. Panic is not a strategy. Precision is.

Key Takeaways

Workers 50 and older can contribute up to $32,500 to eligible workplace plans in 2026, with a higher $35,750 limit for those turning ages 60 to 63 during the year.

Capturing every dollar of employer match is the single highest-return move available to most people, before any other investment or debt strategy.

High-interest consumer debt costs more than most investment returns can earn, making payoff a legitimate catch-up strategy, not a detour from one.

Delaying Social Security beyond full retirement age increases benefits up to age 70, making timing one of the most powerful inflation-adjusted income levers available.

Beginning in 2026, higher-income workers whose prior-year wages exceeded $150,000 may be required to make catch-up contributions on a Roth basis.

The goal is not a perfect retirement plan. The goal is a sturdier financial life, harder to knock over by the surprises that do not send advance notice.

The strange financial weather after 50

For some people, the retirement question gets a confident answer. Accounts funded, employer match captured, home equity building, spreadsheets that behave like obedient pets.

For many others, the answer is more complicated.

Maybe divorce rearranged the furniture of your life. Maybe medical bills ate the savings. Maybe kids, aging parents, job loss, inflation, or sheer exhaustion took priority. Maybe you did save, but not enough.

Maybe you spent 20 years doing everything responsible and still feel like retirement is standing across the river waving a bill.

This is where catch-up strategies after 50 matter. Not because 50 is some magical deadline, the financial industry loves dramatic birthdays because they make excellent marketing scarecrows. But 50 does change the rules in useful ways.

You may qualify for higher retirement contribution limits. You may be in your peak earning years. You may also have less patience for nonsense, which is a severely underrated financial asset.

The real work is less cinematic. It is arithmetic, priorities, debt control, tax awareness, and strategic saving layered with Social Security timing and health care planning.

According to the Federal Reserve’s 2024 household well-being report, only 35% of non-retirees said their retirement savings were on track. EBRI’s 2026 Retirement Confidence Survey found worker confidence fell to 61%, with debt and health care named as the leading obstacles.

Most people reading this are in perfectly ordinary company. The question is what happens next.

The financial question after 50 is not a verdict. It is a starting point.

What “catching up” actually means

Most retirement advice starts with a number. Have six times your salary by 50. Have eight times by 60. Have ten times by retirement.

Helpful? Sometimes. Terrifying? Often. Also a little suspicious, since human lives are not manufactured in matching containers.

A person earning $80,000 with a paid-off house, modest spending, and no dependents may need considerably less than someone earning $150,000 with high housing costs, family obligations, and debt wearing a fake mustache.

Before chasing any generic benchmark, answer four better questions:

- What will your basic retirement lifestyle cost each year?

- What income sources are likely to show up reliably?

- What risks could derail the plan?

- What can you change now without blowing up your life?

That is financial wellness at its most practical. Not yacht fantasy. Not spreadsheet cosplay. Just the ability to make decisions without your nervous system sounding like a smoke alarm.

A catch-up strategy after 50 should not begin with shame. Shame is a terrible financial planner. It never brings receipts.

Maybe you should have done more. Maybe not. Either way, the money does not care. The money only responds to what happens next.

The 2026 catch-up contribution rules: the useful machinery

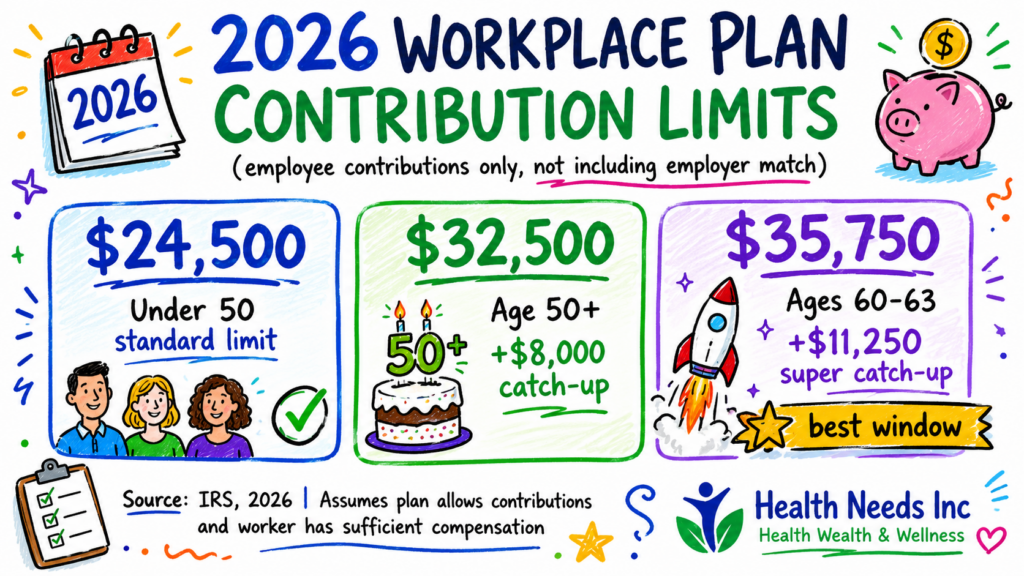

Once you turn 50, the tax code opens a few extra doors. For 2026, the employee contribution limit for eligible workplace retirement plans (401k, 403b, governmental 457, and the federal TSP) is $24,500.

Workers age 50 and older may make an additional catch-up contribution of $8,000, bringing the total to $32,500. According to the IRS, these limits apply across the full range of eligible workplace plans.

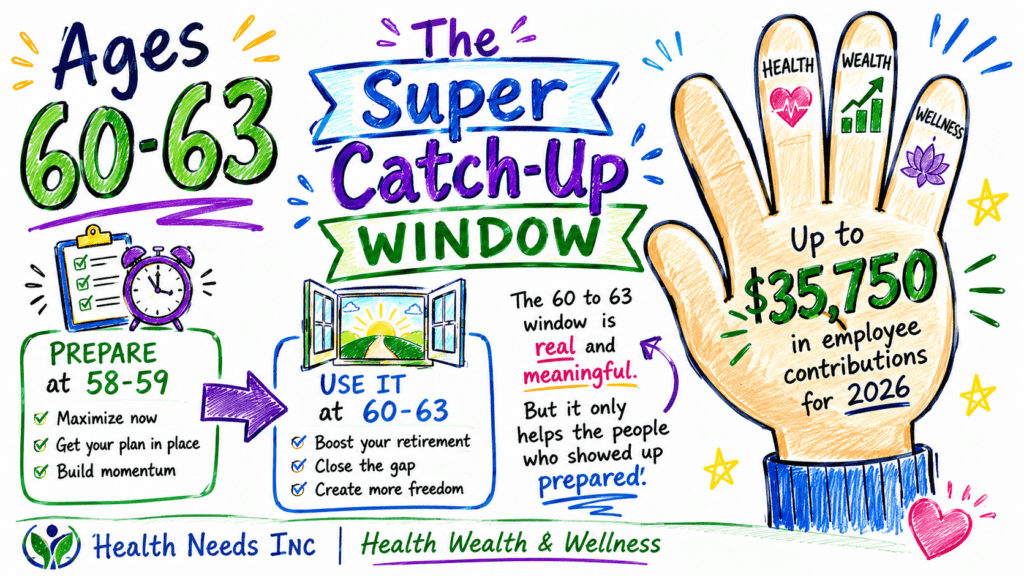

There is also a special higher catch-up for workers who turn ages 60, 61, 62, or 63 during the calendar year. In 2026, that higher amount is $11,250 instead of $8,000. Someone in that age band may contribute up to $35,750 in employee deferrals, assuming the plan allows it.

IRAs have catch-up rules too. In 2026, the IRA contribution limit is $7,500, and people age 50 or older may contribute an additional $1,100, for a total of $8,600 if eligible.

SIMPLE plans: the general limit is $17,000, with a $4,000 catch-up for workers 50 and older.

Workers ages 60 to 63 may qualify for a higher SIMPLE catch-up of $5,250.

The bars get meaningfully taller after 50 and again in the 60 to 63 window.

These numbers matter because the late-game lever is real. You no longer have 35 years of compounding wind at your back. But you may have higher income, fewer child-related expenses, and a stronger ability to focus on the financial picture.

The strategy changes. The opportunity does not disappear.

The employer match, debt triage, and the contribution sequence

The cleanest catch-up move is not heroic. It is automatic.

If you have a workplace retirement plan, increase your contribution rate through payroll. Not someday. Not after you “look at everything,” a phrase that has buried more financial progress than recessions. Start with one percentage point. Schedule another increase in three months. Remove drama from the decision.

Employer match is not a nice perk. It is compensation. If your employer offers a match and you are not capturing all of it, you are leaving part of your paycheck in a corporate drawer. The drawer is wearing khakis, but it is still your money.

High-interest consumer debt is a different matter. Credit card debt is not just a balance. It is a treadmill with a monthly fee and a small whip attached.

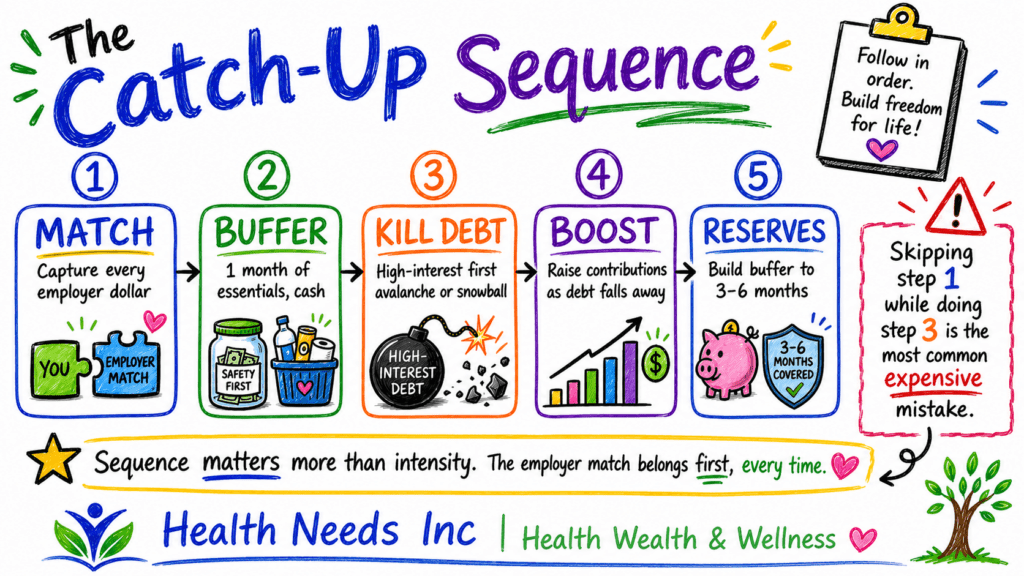

The wrong catch-up strategy is trying to max retirement accounts while carrying expensive revolving debt that compounds in the background. A practical sequence:

The Catch-Up Sequence

Sequence matters more than intensity. The employer match belongs first, every time.

Also worth naming: lifestyle creep. After 50, peak earning years often arrive alongside peak spending years. Home repairs, adult children needing help, medical surprises, subscriptions multiplying quietly in the basement like financial mushrooms.

The goal is not to become cheap. Cheap is just fear wearing a coupon. The goal is conscious spending: find the expenses that do not improve your life, cut those, and automate the savings. Willpower is a flimsy umbrella in a hurricane.

Debt reduction is itself a retirement strategy. Lower fixed expenses in retirement mean your savings do not have to perform circus tricks. As part of a broader retirement planning approach, the sequenced approach above often outperforms chasing maximum contributions while high-interest debt compounds in the background.

The age 60 to 63 super catch-up window

The age 60 to 63 super catch-up provision is one of the more interesting parts of the current retirement system. It is a narrow window, but a powerful one for workers who prepare for it rather than simply waiting to stumble into it.

The danger is treating the super catch-up years as a last-minute rescue helicopter. If you are 58 or 59, do not wait for the window to open before taking action. Prepare for it. Reduce debt. Build cash reserves. Get your investment allocation sensible.

Then, when the larger catch-up window opens, you can actually use it rather than just surviving to it.

The 60 to 63 window is real and meaningful. But it only helps the people who showed up prepared.

A practical staging approach:

- At 58: increase contributions modestly, pay down high-interest debt

- At 59: test whether you can live on less take-home pay without it becoming a crisis

- At 60: push harder into catch-up contributions if cash flow allows

- At 61 to 63: maintain the increased savings rate, resist lifestyle inflation

- At 64: reassess retirement timing, health coverage, Social Security, housing, and income needs

The super catch-up is not magic. Tools work better when used before the house is on fire. The people who benefit most from the 60 to 63 window are the ones who spent 58 and 59 building the capacity to use it.

Roth rules, IRAs, and the HSA as a retirement tool

Beginning in 2026, certain higher-income workers who make catch-up contributions to plans with Roth features may be required to make those contributions on a Roth basis.

According to the IRS, workers whose prior-year wages from a plan sponsor exceeded $150,000 for 2026 will need to direct catch-up contributions to a Roth account rather than a pre-tax one. The upfront tax break disappears for affected higher earners, but qualified withdrawals later may be tax-free.

Whether that is good or bad depends, annoyingly, on your situation. High bracket now, lower bracket in retirement? Losing the pre-tax deduction stings. Expecting higher taxes later, or want more tax diversification? The Roth requirement may actually work in your favor.

The IRA adds another layer. In 2026, people age 50 and older can contribute up to $8,600 to an IRA including the catch-up amount. Over a decade, consistent IRA contributions build meaningful tax diversification, particularly through a Roth IRA if eligible.

Health Savings Accounts deserve more attention than the average steak dinner conversation provides. For 2026, Fidelity summarizes the HSA limits as $4,400 for self-only coverage and $8,750 for family coverage, with an additional $1,000 catch-up for eligible people age 55 or older who are not enrolled in Medicare.

The HSA’s triple tax advantage, possible deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses, makes it one of the most efficient vehicles in the tax code. The catch is eligibility: you need an HSA-qualified high-deductible health plan, and Medicare enrollment ends your ability to contribute.

Late-stage retirement planning is a mosaic. Workplace plan, IRA, HSA, debt reduction, Social Security timing, part-time work, spending changes. No single tile is the whole picture. But remove enough tiles and the image starts to look like a raccoon painted it.

Social Security timing and Medicare planning

Social Security is not just a government check. It is inflation-adjusted lifetime income with survivor benefit components, which makes its timing genuinely important.

According to the Social Security Administration, for people born in 1960 or later, full retirement age is 67. Claiming before full retirement age generally reduces benefits permanently. Delaying beyond full retirement age increases benefits until age 70.

That does not mean everyone should delay. Anyone who says “always delay Social Security” is selling certainty in a world that keeps banana peels on the floor. Health, life expectancy, marital status, survivor benefits, job stability, and household stress all matter.

But for people trying to catch up, delaying Social Security can be one of the most powerful levers if they can afford to wait. Working longer, even part-time, may allow retirement accounts to grow, reduce the number of years those accounts must support, and increase future monthly benefits simultaneously.

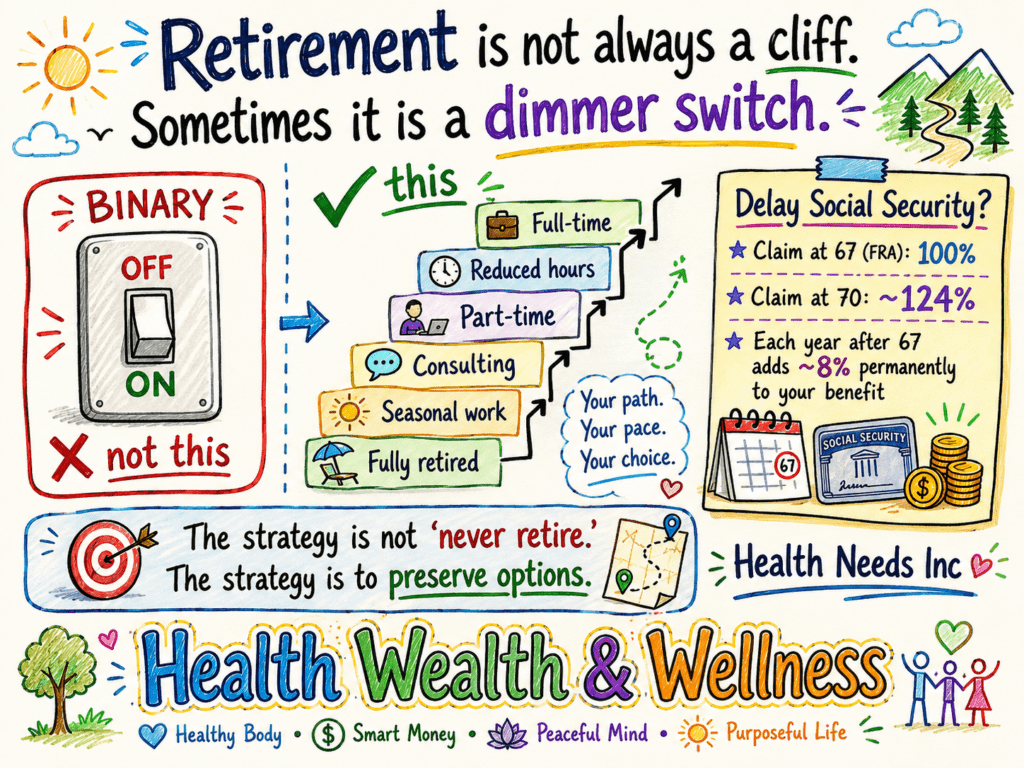

Gradual transitions often outperform hard stops, both financially and psychologically.

Retirement is not always a cliff. Sometimes it is a dimmer switch. OFF ON binary… no

This…

Fully retired… or

Seasonal work… or

Part-time ← Consulting…. or

Full-time?

Delay Social Security?

Claim at 67 (FRA): 100%

Claim at 70: ~124%

Each year after 67 adds ~8% permanently to your benefits

The strategy is not “never retire.” The strategy is to preserve options.

The phrase “work longer” can sound cruel, especially for people in physically demanding jobs. Let’s be precise: the strategy is not simply “never retire.” The strategy is to preserve options.

That might mean staying full-time for two more years. It might mean consulting. It might mean seasonal work. It might mean leaving a toxic job but not leaving paid work entirely. The cognitive and psychological research on purposeful engagement also suggests the binary “working versus retired” framing underestimates the range of choices available.

Medicare eligibility typically begins at 65. If you are delaying Social Security, Medicare does not handle itself automatically. Some people need to sign up separately. Some can delay Part B without penalty if they have qualifying employer group health coverage.

Before 65, review your coverage situation. Are you still working? Is the employer coverage active group coverage? Are you contributing to an HSA? Are you planning to delay Social Security?

Medicare timing affects health costs, HSA eligibility, retirement cash flow, and tax planning. It is boring in the way electrical wiring is boring: nobody celebrates it when it works, but everyone notices when sparks come out of the wall.

Building a retirement income map

Saving is only half the story. After 50, you need to understand future income alongside future expenses. This is where financial planning becomes less about optimization and more about clarity.

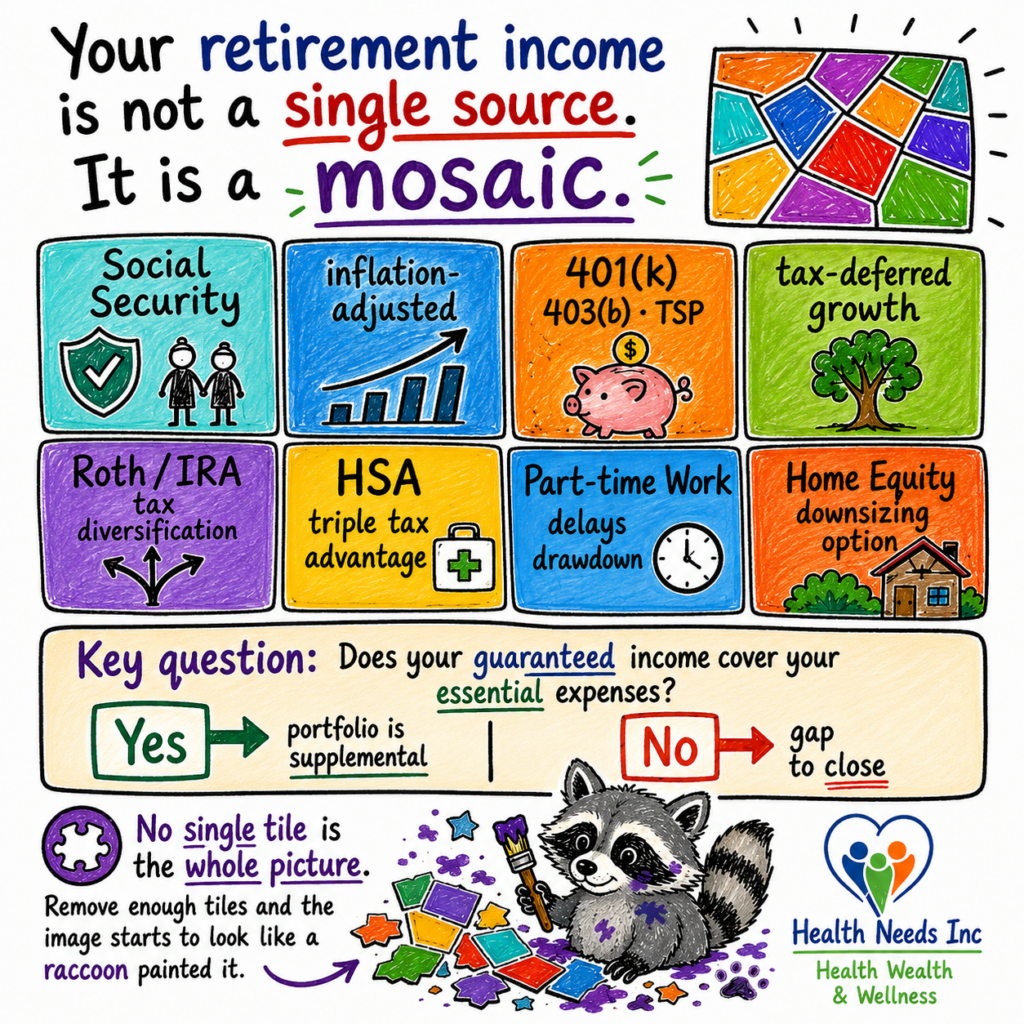

Your retirement income isn’t a single source. It’s diversified…

- Social Security: inflation-adjusted, predictable, yours by right.

- 401(k) / 403(b) / TSP: tax-deferred growth that compounds while you’re not looking.

- Roth / IRA: tax diversification, because future tax rates are nobody’s guess.

- HSA: the triple tax advantage most people forget they have.

- Part-time work: delays drawdown and keeps your brain from arguing with itself.

- Home equity: the downsizing option sitting quietly in your largest asset.

The key question is simple: Does your guaranteed income cover your essential expenses?

If yes, your portfolio is supplemental. You’re playing with house money. If no, you’ve got a gap to close, and that changes every decision downstream

Remove enough tiles and the image starts to look like a racoon painted it.The income map is not a prediction. It is a way to find the weak beams before you move into the house.

Potential retirement income sources

- Social Security benefits (your own, plus survivor or spousal if applicable)

- Workplace retirement accounts (401k, 403b, 457, TSP)

- Traditional and Roth IRAs

- Pensions, if applicable

- Taxable brokerage accounts

- Rental income

- Part-time or consulting work

- Business income

- Home equity options (sale, downsizing, HELOC)

Retirement expenses to estimate

- Housing, utilities, and maintenance

- Food and transportation

- Insurance (health, dental, long-term care, life, auto, home)

- Taxes, both state and federal

- Health care costs beyond insurance, including Medicare premiums

- Travel and discretionary spending

- Family support obligations

- Long-term care risk (statistically significant, often underplanned)

- Fun, because retirement should not be a beige waiting room

Compare guaranteed income to essential expenses. If guaranteed income covers the basics, your investment portfolio has a different job than if there is a gap. This exercise is not meant to predict life perfectly. Life laughs at perfect predictions.

Investment allocation matters here too. Catching up after 50 can tempt people into taking too much risk, which is understandable but frequently counterproductive. High-risk bets can damage late-stage retirement planning because there is less time to recover from major losses.

But excessive caution carries its own risk: inflation can chew through cash like a goat through upholstery. The right portfolio after 50 is not necessarily conservative. It is coherent, meaning it matches your time horizon, risk tolerance, and income needs without requiring perfect timing or emotional numbness.

A 12-month catch-up action plan

Here is a practical first-year roadmap. The goal is momentum over perfection. A working number beats a perfect number that never gets finished.

Months 1 to 2: calculate the gap and gather accounts

Estimate annual retirement spending. List likely income sources. Do not obsess over precision; get a working number.

Then find every retirement account, savings account, debt balance, pension estimate, insurance policy, and Social Security estimate. Put them in one folder. Digital is fine. Paper is fine. Shoebox is emotionally honest but operationally annoying.

Months 3 to 4: increase contributions and build emergency savings

Raise your workplace contribution rate by at least 1%, more if possible. Capture the full employer match.

Simultaneously aim for one month of essential expenses in emergency savings, then build toward three to six months depending on job stability.

Months 5 to 6: attack high-interest debt and review insurance

Use avalanche method (highest interest rate first) or snowball method (smallest balance first). Avalanche saves more interest mathematically. Snowball may build momentum psychologically. Choose the one you will actually follow.

In month 6, review health, disability, life, long-term care options, home, auto, and umbrella liability coverage. Insurance is where financial wellness admits that the universe occasionally throws chairs.

Months 7 to 8: review investments and evaluate IRA and HSA eligibility

Check fees, allocation, diversification, and risk on all accounts. Make sure old accounts are not wandering around unsupervised.

If eligible, decide whether additional IRA or HSA contributions fit your tax and cash-flow picture.

Months 9 to 10: run Social Security scenarios and estimate health care costs

Compare claiming Social Security at 62, full retirement age, and 70. Include spouse or survivor considerations if relevant.

Understand Medicare timing, premiums, supplemental coverage options, and prescription costs. These two months often reveal the biggest planning gaps.

Months 11 to 12: create a retirement income draft and consider professional help

Map which accounts you might draw from first, later, and last. This will change, but the first draft beats financial fog.

If you are within ten years of retirement and uncertain about Social Security timing, Roth versus pre-tax decisions, or how to convert savings into income, consider a fee-only fiduciary financial planner. Ask how they are paid. Ask whether they sell products. Ask what happens if you do nothing. Good advice should be able to defend itself against inaction.

Useful Tools for Catch-Up Planning After 50

- SSA.gov My Social Security free account shows full earnings history and projected benefits at multiple claiming ages

- IRS Retirement Plans page authoritative source for current contribution limits, catch-up rules, and Roth requirement thresholds

- AARP Retirement Calculator models income gaps, spending scenarios, and Social Security timing comparisons

- NAPFA Advisor Search (napfa.org) directory of fee-only fiduciary financial planners searchable by location and specialty

- Fidelity HSA comparison tools compare HSA options, investment menus, and fee structures

- AnnualCreditReport.com free federal access to all three credit bureau reports; useful for the debt triage step

Wellness without the noise.

Evidence-based insights on financial wellness, longevity, and retirement planning. No hype. No spam. Just what works.

No spam ever. Unsubscribe any time.

Final Thoughts

Catch-up strategies after 50 are not just about stuffing more money into accounts. They are about reducing fragility.

Less high-interest debt. More emergency cash. Better tax positioning. A realistic Social Security plan. Investments that do not require clairvoyance. Work options that do not depend on your body behaving like it did in 1989.

Financial wellness after 50 is not about becoming rich in a hurry. That fantasy has ruined plenty of people with perfectly good lives. It is about becoming harder to knock over.

The ability to absorb a surprise without turning it into a catastrophe. The ability to sleep without compound interest standing at the foot of the bed holding a clipboard.

Starting late is not ideal. But it is not nothing. Use the time you have with more precision. Use the IRS rules. Use the catch-up limits. Use the employer match. Use boring automation. Use skeptical thinking when someone in a blazer near a rented yacht offers you a retirement income secret.

The goal is not a perfect retirement. The goal is a sturdier life. That is less glamorous than a yacht. It is also far more useful.

Frequently Asked Questions About Catch-Up Strategies After 50

In 2026, workers age 50 and older can make a standard catch-up contribution of $8,000 on top of the regular $24,500 employee limit, for a total of $32,500 in eligible workplace plans.

Workers who turn ages 60, 61, 62, or 63 during 2026 qualify for a higher catch-up of $11,250 instead of $8,000, bringing their potential total to $35,750. These limits apply to employee contributions and do not include any employer match.

It is not too late. Someone starting at 55 still has meaningful compounding time, access to higher IRS catch-up limits, and the ability to reduce future expenses through debt payoff.

The strategy shifts to using every available lever simultaneously: maximize contributions, capture employer match, reduce high-interest debt, and optimize Social Security timing. Each of these decisions can meaningfully change the outcome.

Beginning in 2026, workers whose prior-year wages from a plan sponsor exceeded $150,000 are generally required to make catch-up contributions on a Roth basis, meaning after-tax rather than pre-tax.

Qualified Roth withdrawals in retirement may be tax-free, but the immediate tax deduction is eliminated for affected higher earners. Whether this helps or hurts depends on your current versus expected future tax rate.

The practical sequence: first, contribute enough to capture any employer match (effectively a guaranteed 50% to 100% return); second, build a small emergency buffer; third, pay off high-interest debt aggressively; fourth, increase retirement contributions as debt falls.

High-interest revolving debt at 20% to 25% APR typically costs more than any realistic investment return, making elimination a legitimate retirement strategy, not a detour from one.

For people born in 1960 or later, full retirement age is 67. Delaying beyond full retirement age increases benefits until age 70, and Social Security is inflation-adjusted lifetime income.

If you can afford to delay by working longer, even part-time, you reduce the number of years your savings must support you while simultaneously increasing your guaranteed monthly income. Health, life expectancy, marital status, and current savings all factor into the decision. The SSA.gov retirement planner models different claiming ages for free.

Yes, if you are enrolled in an HSA-eligible high-deductible health plan and not yet enrolled in Medicare. In 2026, the catch-up contribution for people 55 and older is an additional $1,000 on top of the standard limit.

The HSA’s triple tax advantage makes it one of the most efficient retirement savings vehicles available. The key limit: Medicare enrollment ends your ability to contribute, making the window between 55 and 65 particularly valuable for HSA contributions.

A fiduciary is legally required to act in your best interest rather than their own. Fee-only fiduciary planners charge for their time or a flat fee rather than earning commissions on products they sell.

If you are within ten years of retirement and uncertain about Social Security timing, Roth versus pre-tax strategy, or how to turn savings into income, a good fiduciary planner can be worth the cost. The NAPFA directory at napfa.org and the CFP Board’s search tool are reliable starting points. Always ask how they are paid and whether they have a fiduciary duty in writing.